Four Straight Quarters of Falling Down Payments

The housing market is shifting beneath our feet. After peaking at $30,400 (14.4%) in Q3 2025, the median down payment has slid every single quarter. By Q1 2026, it sat at $23,400, a 19% year-over-year drop, and April 2026's slight uptick to $25,000 is still well below April 2025's $27,500.

To put it in perspective: back in Q1 2019, the median was just $12,500 at 10.7%. What happened in between was a competitive frenzy, low inventory, fast-moving markets, and buyers throwing bigger down payments to win deals. That era is fading in many markets. Inventory has risen year-over-year for 28 consecutive months.

Who Is Actually Buying Right Now?

The buyers returning to the market aren't entering from a place of financial strength, they're stretching to get in. The median buyer FICO score is 733, still healthy, but it's been slipping since late 2025. More importantly, government-backed financing is now carrying a record share of purchase activity.

Key financing shifts

- FHA loans have held above 24% of purchase mortgages for five consecutive quarters, the longest stretch at that level since 2016

- VA loans hit 11.7% in early 2026, their highest share in over a decade

- FHA + VA combined now top one-third of all purchase mortgages

- Conforming loan share has dropped to its lowest level since 2019

One number worth watching closely: mortgage delinquencies are rising, particularly in the FHA segment. Buyers with thinner down payments and softer credit have less buffer if circumstances change.

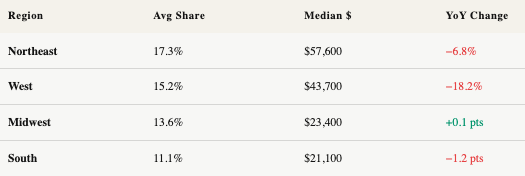

Breaking It Down by Region

Down payment trends aren't uniform. Where you work, or where you're buying, dramatically changes what this data means for you.

The Northeast remains the most competitive market in the country, with buyers putting down 17.3% on average, up a staggering 236.8% since Q1 2019. The Midwest is the only region where down payment share ticked up year-over-year. Meanwhile, the South and West have recovered more inventory, giving buyers room to breathe and negotiate.

Notably, the South and Midwest now account for more than 71% of all U.S. home sales, meaning more transactions are happening in lower down-payment markets, which pulls the national average down.

What This Means for Buyers

If you're a renter thinking about buying, the math is more accessible than many realize, but the path matters:

- The typical renter has $2,600–$2,900 in accessible assets

- About 15–20% of renters could cover the $23,400 conventional median

- About 20–26% could clear the FHA threshold of ~$14,875 on a median-priced home

FHA and VA loans aren't a fallback, for millions of qualified buyers, they're the front door into homeownership right now.

What This Means for Sellers

The buyer pool is real, but it looks different. Nearly 40% of sellers now expect to make concessions — up from 30% in 2025. Pricing strategy and flexibility on closing costs or repairs will matter more this spring and summer than they have in years.

The Real Test: Spring and Summer 2026

If down payments don't climb back toward the 14–15% range by summer, the softening many agents are observing isn't a temporary blip, it's the new baseline. Agents who adapt their client conversations now, especially around FHA/VA financing and realistic seller expectations, will be far better positioned heading into the second half of the year.

Check out this article next